The Hidden ROI of Fleet Safety

Fleet accidents cost U.S. businesses over $150 billion annually in direct and indirect costs, and that figure doesn’t account for the long-tail expenses that never show up on an accident report: the driver who never returns to full productivity, the contract lost because a delivery didn’t arrive, the lawsuit that settles three years later.

For most fleet managers, safety programs live in the budget as a cost. Training hours, monitoring hardware, compliance software, all of it feels like spending with no obvious return line. But insurers see it differently. To an underwriter, a fleet with documented safety systems, clean driver records, and low claims frequency is simply a better risk. And better risks get better rates.

This article unpacks that gap between perception and reality. It covers how insurers actually price fleet risk, which safety investments have the most measurable impact on premiums, which tools are worth deploying, and how to make the financial case to leadership. The core argument is straightforward: learning how to reduce insurance costs through fleet safety is not a side benefit of running a safer operation. It is one of the most reliable returns available to a fleet manager willing to be proactive.

Why Insurance Costs Are Rising for Fleet Operators

Fleet insurance is getting more expensive, and it is not slowing down. Commercial auto premiums have risen for over a decade consecutively, with some segments of the trucking and logistics industry seeing double-digit increases at renewal. For fleet operators already working on thin margins, this is not an abstract trend. It is a line item that grows every year without any obvious way to fight back.

Several forces are driving this. Accident frequency in commercial fleets has climbed alongside the explosion in last-mile delivery demand, putting more vehicles on the road under tighter time pressure than ever before. When accidents do happen, they are more expensive to resolve. Repair costs have surged due to the advanced sensor systems and materials in modern vehicles. Medical costs have followed a similar trajectory. And in the United States in particular, nuclear verdicts, jury awards in the tens or hundreds of millions against trucking companies, have fundamentally changed how insurers calculate liability exposure for commercial fleets.

Distracted driving has added another layer of risk that traditional underwriting models were not built to handle. Smartphones, in-cab navigation systems, and dispatch communications all compete for a driver’s attention in ways that were not a serious actuarial concern twenty years ago.

The result is that insurers are becoming significantly more selective. Fleets with poor safety records are increasingly facing coverage restrictions, higher deductibles, or outright non-renewals. More importantly, underwriters are moving away from broad industry averages and toward individualized, data-driven risk assessment. They want telematics reports, incident trend histories, driver behavior scores, and documented safety program records before they quote. Your safety posture has become a pricing signal, and it is being read whether you are managing it deliberately or not.

How Insurers Actually Calculate Fleet Risk

Most fleet managers know that accidents push premiums up. Fewer understand the full picture of how underwriters arrive at a number, which means they miss opportunities to influence it. Insurance pricing for commercial fleets is not a black box, it is a structured assessment of several measurable risk factors. Understanding each one is the first step toward actively managing them.

Loss Ratio and Claims History

Your claims history is the single heaviest factor in your premium calculation. Insurers look at both frequency, how often claims occur, and severity, how much each one costs to resolve. A fleet with several small claims can be penalized just as heavily as one with a single catastrophic event, because frequency signals a systemic safety problem rather than bad luck. Most insurers look back three to five years, meaning a poor safety period follows a fleet long after the underlying problems have been fixed.

Driver Risk Profiles

Insurers do not just assess your fleet as a whole. They score drivers individually using Motor Vehicle Records, years of licensed experience, prior violation history, and in some cases, results from driver assessments or training programs. The overall composition of your driver pool shapes your aggregate risk score significantly. A single high-risk driver on your roster can affect the rate applied across the entire fleet, which is why driver qualification and ongoing monitoring matter beyond safety alone.

Vehicle Type, Age and Maintenance Records

The vehicles themselves carry their own risk profile. Older vehicles without modern safety features such as automatic emergency braking, lane departure warnings, or stability control represent higher mechanical and collision risk in the eyes of an underwriter. Documented preventive maintenance schedules work in a fleet’s favor because they demonstrate that mechanical failure risk is being actively managed rather than left to chance.

Safety Program Documentation

Increasingly, insurers are offering measurable discounts for fleets that can demonstrate formal, verifiable safety programs. The keyword here is verifiable. A verbal assurance that drivers are trained is worth very little at renewal. A documented program with training records, incident review logs, policy acknowledgments, and regular safety audits is a tangible asset that underwrites can price against. If your safety program exists but is not being documented, you are leaving money on the table.

The Direct Link Between Fleet Safety and Lower Premiums

Understanding how insurers calculate risk is useful. Knowing what actually moves the needle on your premium is where that knowledge becomes actionable.

The evidence is consistent across the industry: fleets that implement structured, measurable safety programs reduce accident rates by 20 to 40 percent over time. Fewer accidents mean fewer claims. Fewer claims mean a better loss ratio. A better loss ratio at renewal means real, quantifiable reductions in what you pay. This is not a theory. It is the core mechanic of how commercial insurance pricing works, and it rewards proactive fleets directly.

Telematics has accelerated this dynamic significantly. Many insurers now offer usage-based insurance programs that price premiums based on actual driving behavior data rather than historical averages. Fleets that share telematics data demonstrating safe driving patterns, controlled speeds, smooth braking, and low incident frequency can access discounts ranging from 10 to 25 percent compared to fleets priced on industry benchmarks alone.

Driver training delivers similarly measurable results. Fleets with documented, recurring defensive driving programs have reported reductions in at-fault collisions of up to 30 percent within the first year of implementation. That kind of improvement, sustained over two or three renewal cycles, compounds into premium reductions that dwarf the original cost of the training program.

There is also a less obvious financial benefit worth highlighting: subrogation. When an accident is not your driver’s fault, a well-documented fleet with strong incident response protocols is far better positioned to recover costs from the at-fault party’s insurer. Effective subrogation reduces your net claims exposure even in accidents you did not cause.

The Compounding Effect

The most powerful argument for fleet safety investment is not what it saves you this year. It is what it saves you over time. Lower claims produce a better loss ratio. A better loss ratio earns a lower base rate at renewal. A lower base rate frees up budget that can be reinvested into safety infrastructure. That infrastructure reduces claims further. Each cycle reinforces the next.

To make this concrete: consider two fleets of identical size and vehicle type. Fleet A runs no formal safety program and files an average number of claims each year. Fleet B invests in telematics, driver training, and incident documentation, and reduces its claim frequency by 25 percent over three years. By the third renewal, the premium gap between those two fleets can represent tens of thousands of dollars annually, a figure that grows with fleet size.

Key Fleet Safety Measures That Insurers Reward

Knowing that safety reduces premiums is one thing. Knowing which specific investments carry the most weight with underwriters is what turns that knowledge into a procurement decision. The following measures are not just best practices in the abstract. They are the ones insurers most consistently recognize, document, and reward at renewal.

1. Telematics and Real-Time Driver Monitoring

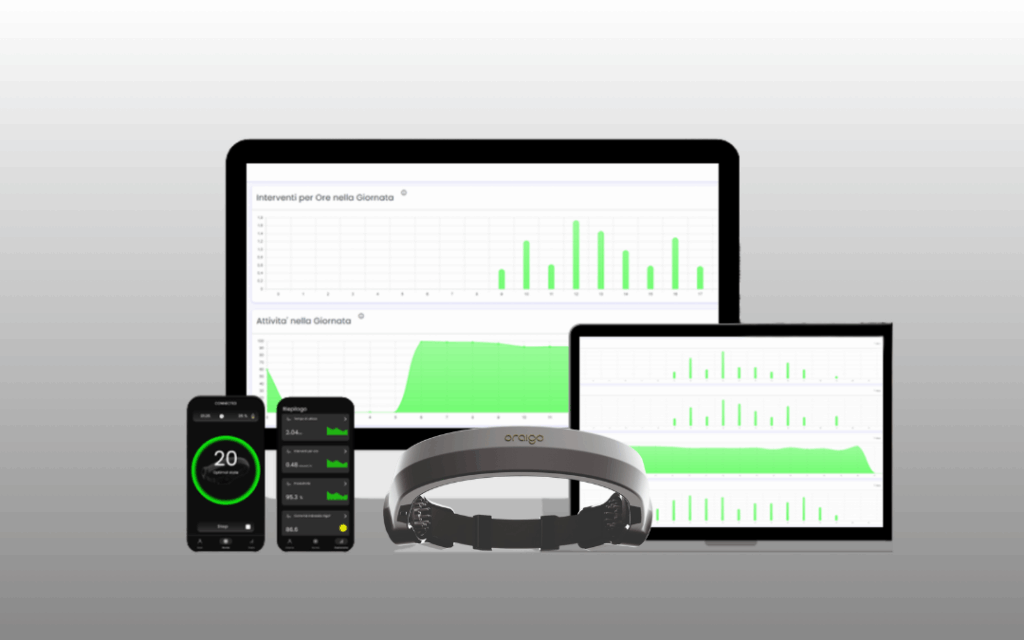

Telematics platforms are the foundation of a modern fleet safety program. By tracking speeding events, harsh braking, rapid acceleration, cornering behavior, and idle patterns, telematics gives fleet managers a continuous, objective picture of how every driver operates every day.

The insurance benefit is twofold. First, the data enables proactive coaching that changes behavior before accidents happen. Second, many insurers now accept telematics reports directly as part of the underwriting process, using real driving behavior rather than historical claims averages to set rates. Fleets that can demonstrate consistently safe driving data across their entire pool are in a strong negotiating position at renewal.

2. Dashcams and Event Recorders

Dashcams have become one of the most cost-effective safety investments available to fleet operators, particularly because their insurance benefit is immediate and concrete. Dual-facing cameras that capture both the road ahead and the driver’s behavior create an objective record of every incident, eliminating the ambiguity that makes claims expensive and slow to resolve.

Fraudulent claims, staged accidents, and exaggerated injury allegations are a growing problem for commercial fleets. Video evidence shuts these down quickly, often before litigation begins. Beyond fraud protection, dashcam footage accelerates legitimate claims resolution, reduces legal fees, and in many cases shifts liability determinations that would otherwise have gone against the fleet. A number of insurers now offer explicit premium credits for dashcam-equipped vehicles precisely because the data reduces their own exposure.

3. Driver Fatigue and Distraction Monitoring

Fatigue and distraction together account for a disproportionate share of serious commercial fleet accidents, and they are also among the hardest risks to manage through scheduling or policy alone. A driver can be fully compliant with hours-of-service regulations and still be dangerously fatigued due to poor sleep quality, circadian disruption, or underlying health factors.

Advanced monitoring tools address this gap directly. AI-powered camera systems detect visible signs of drowsiness such as slow blinking, head nodding, and yawning, and trigger real-time alerts before a microsleep event occurs. EEG-based wearable systems go a step further, measuring neurological indicators of fatigue at the source, often identifying impairment before any visible behavioral sign appears.

For insurers, fleets that deploy fatigue and distraction monitoring demonstrate something that goes beyond compliance. They demonstrate active duty of care, a documented commitment to intervening before accidents happen rather than simply reporting them afterward. That posture matters both in premium negotiations and in liability defense if an accident does occur.

4. Formal Driver Training and Certification Programs

Documented, recurring driver training is one of the most straightforward ways to signal reduced risk to an underwriter. Defensive driving courses, load safety training, hours-of-service compliance programs, and incident response drills all contribute to a driver pool that is measurably less likely to generate claims.

The emphasis must be on documentation. Training that happens but is not recorded, certified, or traceable provides no underwriting value. Fleets should maintain individual training records for every driver, track completion rates, and schedule refresher programs at regular intervals. Some insurers maintain formal partnerships with approved training providers and offer direct premium credits for completed certifications.

5. Preventive Vehicle Maintenance Programs

Mechanical failure is a claims category that insurers weight heavily because it is, in most cases, entirely preventable. A documented preventive maintenance schedule, with service records attached to each vehicle in the fleet, signals to underwriters that this category of risk is being actively managed.

Driver Vehicle Inspection Reports completed before and after each shift create an additional auditable trail. When a fleet can demonstrate that vehicles are inspected daily, serviced on schedule, and that defects are logged and addressed promptly, it removes a meaningful source of uncertainty from the underwriting equation.

6. Incident Response and Reporting Protocols

How a fleet responds to accidents matters almost as much as how often they happen. A formal incident response protocol that ensures accurate documentation, prompt reporting, driver support, and evidence preservation consistently produces better claims outcomes than an ad hoc approach.

Fast, thorough reporting reduces claims costs by limiting the window for evidence to degrade or narratives to shift. A structured Return-to-Work program for injured drivers reduces workers’ compensation exposure and signals to insurers that the fleet manages the full lifecycle of an incident, not just the immediate aftermath.

How to Make the Business Case Internally

For many fleet safety managers, the hardest conversation is not with an insurer. It is with a CFO or operations director who sees a budget request for monitoring hardware, training programs, and compliance software and wants to know what the return looks like in concrete terms.

The most effective framing is not safety. It is total cost of risk.

Total cost of risk, often abbreviated as TCOR, captures the full financial exposure of running a fleet without adequate safety investment. It includes insurance premiums, yes, but also direct claims costs that fall within the deductible, legal fees, settlement costs, vehicle downtime and replacement, driver turnover driven by accident-related attrition, and the administrative burden of managing incidents after the fact. When all of these are added together, the true cost of an unsafe fleet is almost always significantly higher than the line item for safety program investment.

The calculation does not need to be precise to be persuasive. Start with your fleet’s current cost per mile for insurance and multiply it across your annual mileage. Then model a conservative 15 percent reduction in that figure, the kind of improvement that a well-documented telematics program and driver training initiative can realistically deliver within two renewal cycles. Present that delta alongside the cost of the safety investment required to achieve it. In most fleets of meaningful size, the payback period is measured in months, not years.

It also helps to bring your insurance broker into this conversation early. A good commercial fleet broker can provide indicative data on the premium impact of specific safety measures before you commit to purchasing them. That external validation carries weight in internal budget discussions in a way that internal advocacy alone often does not.

Finally, quantify the downside of inaction. A single at-fault accident involving a serious injury can generate a claim that affects your premium for five years and, in a nuclear verdict scenario, threatens the financial viability of the business entirely. Safety investment is not just a way to reduce costs. It is a way to put a ceiling on catastrophic exposure, and that argument tends to land with leadership in a way that incremental premium savings sometimes do not.

Working With Your Insurer to Reduce Costs

Most fleet operators engage with their insurer once a year at renewal, review the quoted premium, and either accept it or shop it to competitors. That passive approach leaves significant savings unrealized. The fleets that consistently achieve the best insurance outcomes treat their insurer and broker as active partners in risk management, not just vendors they transact with annually.

The single most important shift is timing. Do not wait for renewal to share evidence of your safety program’s progress. Mid-term updates that document telematics improvements, training completion rates, reduced incident frequency, or the deployment of new monitoring technology keep your underwriter informed and on record as having received that information. When renewal arrives, the conversation starts from a position of demonstrated performance rather than a blank slate.

Be explicit about what you are asking for. Many insurers offer loss control credits, safety program discounts, and telematics-based pricing adjustments that are not automatically applied. They are available to fleets that ask for them and can substantiate the request with data. Your broker should know what each insurer on your panel offers in this area, and if they do not, that is worth addressing directly.

Request a formal loss control consultation if your insurer offers one. Many commercial carriers provide complimentary risk engineering visits where a specialist reviews your operations, identifies exposure areas, and recommends improvements. Beyond the operational value, these consultations signal to the underwriter that your fleet is engaged and proactive, a posture that influences how your account is treated at renewal.

Benchmarking is another underused tool. If your fleet’s loss ratio is performing better than the industry average for your vehicle class and geography, make that case explicitly. Underwriters work with averages by default. A fleet that can demonstrate it is outperforming those averages has a legitimate basis to push back on rate increases that are driven by market trends rather than its own claims history.

The broader point is that insurance pricing is not purely mechanical. Relationships, communication, and the quality of the information you provide all influence outcomes. Fleets that are easy to underwrite, transparent with data, and consistent in their safety efforts are the ones that carriers want to retain, and retention appetite translates into pricing flexibility.

Building a Culture of Safety That Sustains Results

Every tool and program covered in this article depends on one thing to deliver lasting results: drivers who are genuinely engaged with safety rather than merely compliant with it. Technology can monitor behavior. Policies can mandate it. But neither can manufacture the kind of consistent, day-to-day commitment that actually moves claims numbers over time. That comes from culture, and culture is built deliberately or not at all.

The foundation is trust. Drivers who understand why monitoring systems exist, how their data is used, and what protections are in place around it are far more likely to engage with safety programs constructively. Introducing telematics or fatigue monitoring as a surveillance tool breeds resentment and workarounds. Introducing it as a system that protects drivers from false liability claims, supports them after incidents, and helps the company invest in their wellbeing produces a fundamentally different response.

Recognition programs are one of the most cost-effective cultural levers available. Safe driver awards, milestone bonuses for clean records, and public acknowledgment of safety performance signal to the entire workforce that safe behavior is valued and visible. Incentive structures do not need to be expensive to be effective. Consistency and sincerity matter more than the size of the reward.

Equally important is how safety expectations are enforced when delivery pressure spikes. The moments that define a safety culture are not the easy ones. They are the moments when a manager has to choose between pushing a fatigued driver to meet a deadline and pulling them off the route. Fleets where leadership consistently makes the right call in those moments build a reputation internally that no policy document can replicate. Drivers notice, and they respond accordingly.

Finally, safety culture requires feedback loops. Drivers should receive regular, specific feedback on their performance scores, not just a notification when something goes wrong. Coaching conversations that acknowledge improvement, not just violations, build the kind of ongoing engagement that sustains behavioral change over months and years rather than spiking after an incident and fading quietly afterward.

Safety as a Financial Strategy: Reduce Insurance Costs Through Fleet Safety Investments

Fleet safety and insurance cost reduction are not parallel tracks that occasionally intersect. They are the same track. Every investment in driver monitoring, vehicle maintenance, training documentation, and incident response is simultaneously an investment in a lower premium, a stronger negotiating position at renewal, and a smaller ceiling on catastrophic financial exposure. The fleets that understand this are not just safer. They are more profitable, more insurable, and more resilient when things go wrong.

The practical steps are clear. Audit your current safety program honestly and identify where documentation gaps exist. Engage your broker in a direct conversation about which specific measures your insurers reward and what evidence they need to see. Deploy telematics and monitoring tools that generate the kind of objective, continuous data that modern underwriters respond to. Train your drivers consistently and record every session. Build the internal business case using total cost of risk, not just premium line items, and present it to leadership before the next renewal forces the conversation.

None of this requires a complete operational overhaul. The fleets that see the greatest insurance improvements are rarely the ones that launched the most ambitious safety initiative. They are the ones that made steady, documented progress over two or three renewal cycles and showed up to each negotiation with evidence rather than assurances.

The insurance market is moving in one direction. Underwriting is becoming more data-driven, more individualized, and less forgiving of fleets that cannot demonstrate active risk management. The gap in premium between a safety-mature fleet and an average one will continue to widen. That gap is either a cost you absorb or an advantage you build. The decision about which one it becomes is made not at renewal, but in the daily operational choices that either generate safety data worth sharing or quietly add to a claims history that follows your fleet for years.

The business case for fleet safety has never been stronger. The only question is how long to wait before acting on it.

Ready to reduce insurance costs through smarter fleet safety?

Oraigo’s real-time brainwave monitoring technology helps fleets prevent accidents before they happen, giving you the safety data insurers reward. Protect your drivers, lower your risk profile, and take control of your premiums.

Book a free consultation with one of our specialists today.